February 28, 2026. Everything Changed Overnight.

It began, as so many crises do, with a headline that seemed impossible. US-Israeli strikes on Iran. The GCC’s airspace fractured within hours. Missiles fell on UAE territory for the first time since the 1980s. By the time markets opened the next morning, roughly $120 billion had been erased from UAE exchange and the region’s ten-million-strong expatriate community was asking a question nobody wanted to answer: should I stay?

The financial shockwaves were real and measurable. But what followed over the next six weeks was a quieter, more personal reckoning playing out in living rooms, WhatsApp groups, supermarket aisles, and HR offices across Dubai, Abu Dhabi, Sharjah, Riyadh, Jeddah, and Dammam.

A recent resident sentiment study by Borderless Access across the UAE and Saudi Arabia with 421 respondents drawn from locals, expat Arabs, expat Asians, and expat Westerners reveals the harsh reality. Spanning every income band from ABC1 to C2, the study reveals a more nuanced shift in consumer behavior beneath the visible economic shock triggered by the February 2026 conflict. The findings are something brands cannot afford to ignore.

One Region, Multiple Realities

If there is one number from this consumer behavior research that every brand, employer, and policymaker in the region should print and pin to their wall, it is this: 53% of residents are currently anxious. But that average masks an enormous geographic fault line.

Dubai is the epicentre. Nearly a quarter of its residents describe themselves as ‘very anxious or stressed’ — a figure that towers above every other city in the survey. The UAE overall registers 54% anxiety versus KSA’s 52%, but the city-level story is far more dramatic. Jeddah comes close to Dubai at 25%, while Riyadh and Dammam sit considerably lower.

The divergence is structural, not psychological. KSA’s oil-anchored economy acts as a shock absorber. The UAE — and Dubai in particular — is a city built on connectivity, openness, and international flows of capital, talent, and tourism. When those flows are disrupted, Dubai feels it first and feels it hardest.

The wellbeing gap tells the same story. Across every city surveyed, residents report more worsened wellbeing than improved — but Dubai and Jeddah each sit at -27 points, the deepest declines in the survey. On safety perception, the gap between KSA (88% feeling safe) and UAE (78%) is a ten-point chasm with real commercial implications.

Consumers are not withdrawing completely. Instead, they are becoming more deliberate and are weighing in their purchases more carefully. This creates a new kind of consumer sentiment, one that is cautious, observant, and highly responsive to changes in price, availability, and perceived value.

Expats Shoulder More. Older Residents Feel It Differently.

Anxiety, it turns out, has gripped everyone irrespective of nationality, age, and financial exposure.

The study shows that expats experience significantly higher levels of anxiety than locals, reflecting concerns around job security and long-term stability. These consumer behavior insights also reveal that younger individuals, more exposed to uncertainty and future planning pressures, report higher emotional stress.

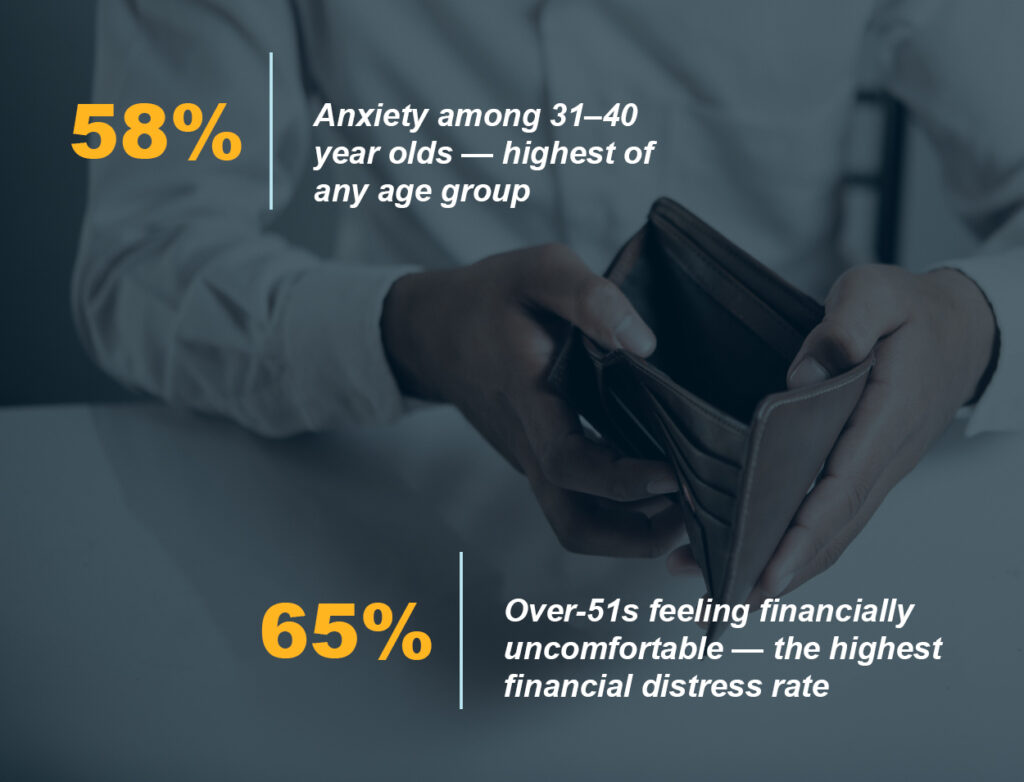

Age splits the experience further. The 31–40 cohort is the most anxious group at 58% — a generation juggling young families, career decisions, and the dawning possibility that the city they chose to build their life in might not feel as safe as it once did. But go past 51, and anxiety drops sharply. Only 31% in that bracket are anxious. What replaces it, however, is financial discomfort: 65% over the age of 51 years say they feel financially uncomfortable, the highest rate of any age group.

These differences matter as they shape how people spend, plan, and develop relationships with brands. A minor adjustment for one group may represent a major lifestyle shift for another.

For brands, this reinforces the need to move beyond broad segmentation and toward a more layered understanding of consumer realities.

Consumer Behavior in Times of Uncertainty

Here is where the survey delivers its most counterintuitive finding, and the one that should matter most to anyone making strategic decisions in this region: despite everything, optimism persists.

51% of residents are optimistic about the economic outlook over the next 12 months. 53% expect their personal finances to improve. KSA leads both figures — 54% optimistic, 57% expecting personal improvement. But even UAE, the harder-hit market, is not capitulating. This is the paradox: the GCC consumer can hold anxiety and hope simultaneously, in the same breath, without apparent contradiction.

The job security picture is more fragile. Only 20% of residents overall feel secure in their jobs, falling to just 15% in the UAE. Expats feel considerably less secure than nationals — a finding the report flags as a structural talent risk for employers. In response, 30% of residents are actively saving more than before, suppressing discretionary spending and reshaping category volumes in ways that will outlast the immediate crisis.

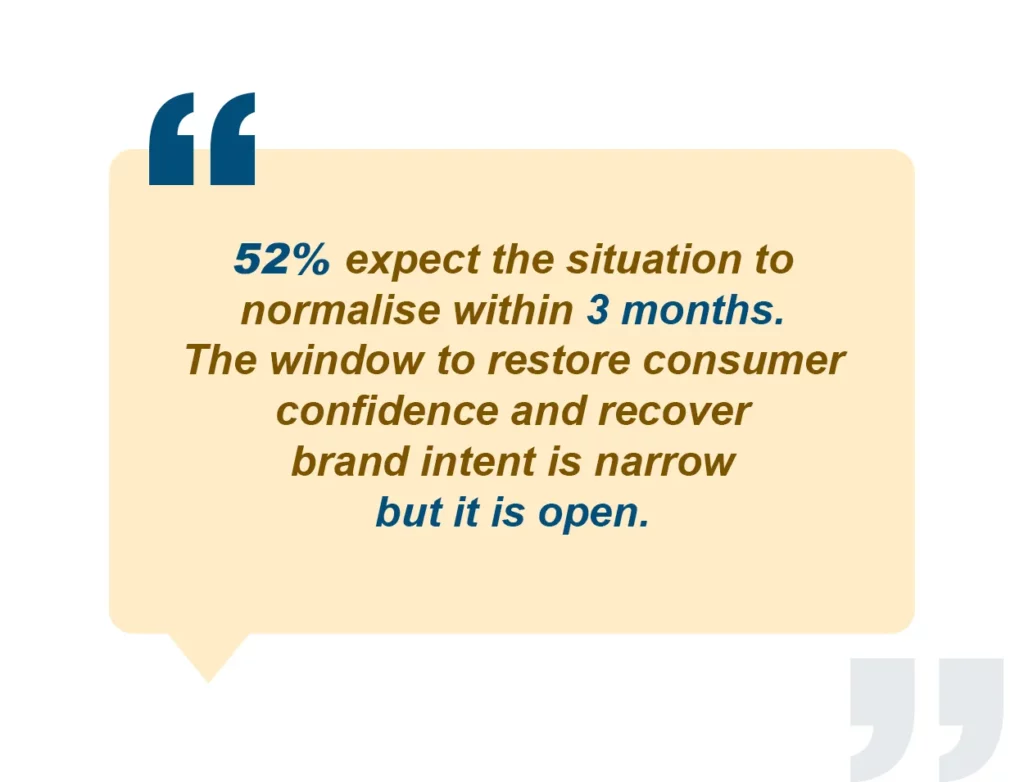

The fact that 52% are expecting normalization within three months is arguably one of the most important findings in the entire report. It means the recovery window is real and consumer habits have not yet calcified. Brands that move in this window have a genuine chance to recover the ground they are losing. Brands that wait may find new habits have already locked in.

The Spending Behavior is Being Rewired

One of the clearest expressions of the uncertainty is visible in how people are spending.

Discretionary categories—entertainment, dining, fashion—are seeing the steepest footfall reduction — up to 62% of UAE residents report visiting entertainment parks less frequently. Restaurants are down (51% fewer visits in UAE). Malls are quieter (56% reporting reduced visits).

At the same time, essential spending has taken on new urgency.

Food and beverage purchases have risen significantly—by nearly 28%—partly driven by stockpiling behavior as consumers prepare for potential disruptions. Three quarters of UAE residents admit to stockpiling behaviour, a pattern the region last saw in the early days of the pandemic

The supply chain effects are no longer abstract. 60% of residents say prices of essential goods have risen since the conflict began — rising to 74.8% in the UAE and a striking 88.4% in Dubai specifically. The Strait of Hormuz disruption has made its way directly into the weekly shop. Strait-related import cost increases are visible on shelves, and residents can feel them.

Loyalties That Took Years to Build Are Shifting in Weeks

This is where the survey moves from sociology to commercial urgency. Purchase intent is declining across every category — F&B, QSR, fashion, electronics, beauty, home care. But the pattern within that decline is deeply uneven, and it is not random.

Global brands are losing ground faster than local alternatives. In the QSR category, international chains are haemorrhaging intent points: Starbucks at -29, McDonald’s at -21, KFC at -23. Meanwhile, local Saudi brands like ALBAIK hold at 0 — no decline at all. In home care, local detergent lines are the only measured brand holding positive net intent (+2 points), while multinationals from P&G, Reckitt, Henkel, and Unilever are all in negative territory.

Price and availability are the primary engine of this shift — 31% cite these as the key reasons for changing consumer behavior. Supply disruptions and perceived price hikes are pushing consumers toward whatever is cheaper and actually on the shelf. But geopolitical stance is an emerging secondary driver, particularly in the UAE, adding a harder ideological edge to what might otherwise look like purely economic switching.

The duration data is what should keep brand leaders awake. 17% say their preferences have permanently changed. 20% say the change will persist for 6–12 months after resolution. A further 30% are unsure — which, at scale, represents an enormous cohort of consumers whose habits are still forming. The brands that show up for them in the next 90 days may well define the next several years of market share.

What Brand Leaders Need to Do Right Now

The survey does not end with diagnosis. It ends with direction. Six strategic implications emerge from the data — each one concrete, time-bound, and actionable:

1. Never aggregate UAE. Dubai — 60% anxious, 88% perceiving price rises, stock market down 16% — is a fundamentally different market from Abu Dhabi or any KSA city. Country-level strategies will systematically underserve the most stressed consumer base in the region.

2. The 90-day recovery window is open — act now. 52% expect normalisation within 3 months. The 30% ‘unsure’ segment on brand permanence is the most addressable group in the market right now. Brands that engage in this window have the best chance of recovering intent before new habits lock in.

3. Lead with price and supply assurance. Purpose-led messaging will be outgunned right now. Supply chain transparency, competitive pricing, and product visibility will outperform cause-led campaigns in the short term. Show up on the shelf. Show up in the wallet.

4. Track UAE expats as the leading recovery indicator. This demographic — the UAE’s largest — shows the highest anxiety, the deepest discretionary pullback, and the highest relocation consideration. Their confidence is the single best forward indicator of category volume recovery.

5. Defend shelf presence in F&B and Home Care. Net intent in F&B is near-neutral — not yet lost. The real risk is a quiet, gradual drift to local alternatives via availability and price. Prioritize in-store visibility and supply reliability over promotional discounting.

6. Cross-reference your Net Intent Score against switching drivers. Brands with strongly negative NIS, a ‘permanently changed’ signal, and ‘geopolitical stance’ as the primary driver face the hardest recovery and may require genuine repositioning — not just a spend increase.

A Region That’s Anxious but Not Broken

The 421 residents who took part in this survey did not speak with one voice. They spoke from six cities, four nationalities, multiple income bands, and the full complexity of consumer behavior in genuinely uncertain times. What they shared, above all, was the same stubborn refusal to give up. For the brands and institutions that serve them, that refusal is both a warning and an invitation.

The Gulf has weathered shocks before. Oil price crashes, the 2008 financial crisis, a global pandemic. Each time, the region’s resilience surprised those who had written it off too quickly. This survey suggests that instinct is still alive in 2026.

The brands and businesses that act with speed, precision, and genuine understanding of what people in this region are actually experiencing right now will be the ones still standing when the dust settles.

This article covers selected highlights. The full report includes city-level breakdowns, category-by-category Net Intent Score data, demographic crosstabs across 15+ sectors, and detailed strategic implications.

↓ Download the Full Report Here